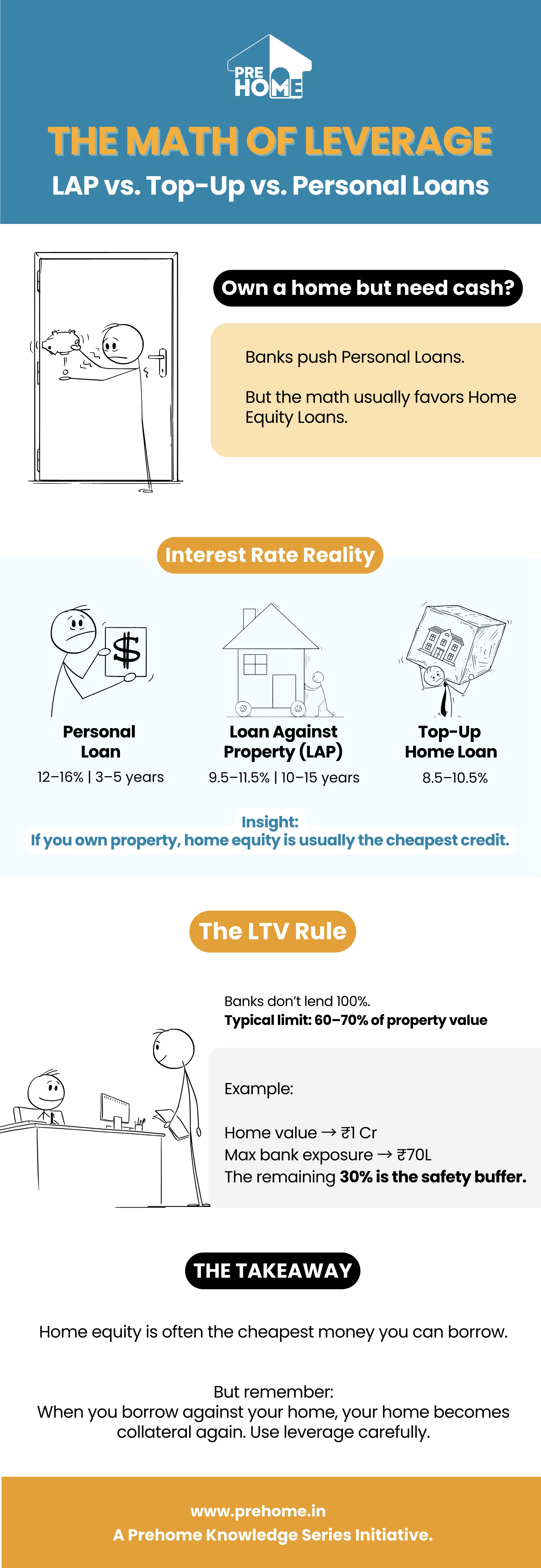

You now know your equity isn't dormant; it's waiting (Blog 37) . But banks seldom promote Home Equity products. Instead, they push pre-approved Personal Loans. Why is that? Because the math favors the bank with personal loans and favors you with a home equity loan. Let’s break down the numbers.

When you borrow money, the interest rate shows how risky it is for the bank.

Don't expect the bank to give you 100% of your equity

This is where smart people lose their homes. Behavioral psychology warns us about Mental Accounting—the habit of treating different money sources with unequal value. Homeowners often see equity as "lottery money" or a bonus, instead of as hard-earned wealth.

The math shows home equity is the cheapest money you can borrow. But cheap money is also the easiest to waste. When you borrow against your home, the asset becomes collateral again. If you fail to repay, the bank's claim takes precedence over your emotional ties. This is why leverage should always serve productive or stabilizing purposes.

We’ve examined interest rates and psychological traps. Now, let’s see how the top 1% actually use this strategy in the real world. Blog 39 Smart Moves: How to Use Home Equity to Build Wealth