Theory means little without action. We know the tools (Blog 37) and we understand the math (Blog 38 - The Math of Leverage: LAP vs. Top-Up vs. Personal Loans). Now, let's look at how savvy investors use their home equity to grow their wealth without taking excessive risks.

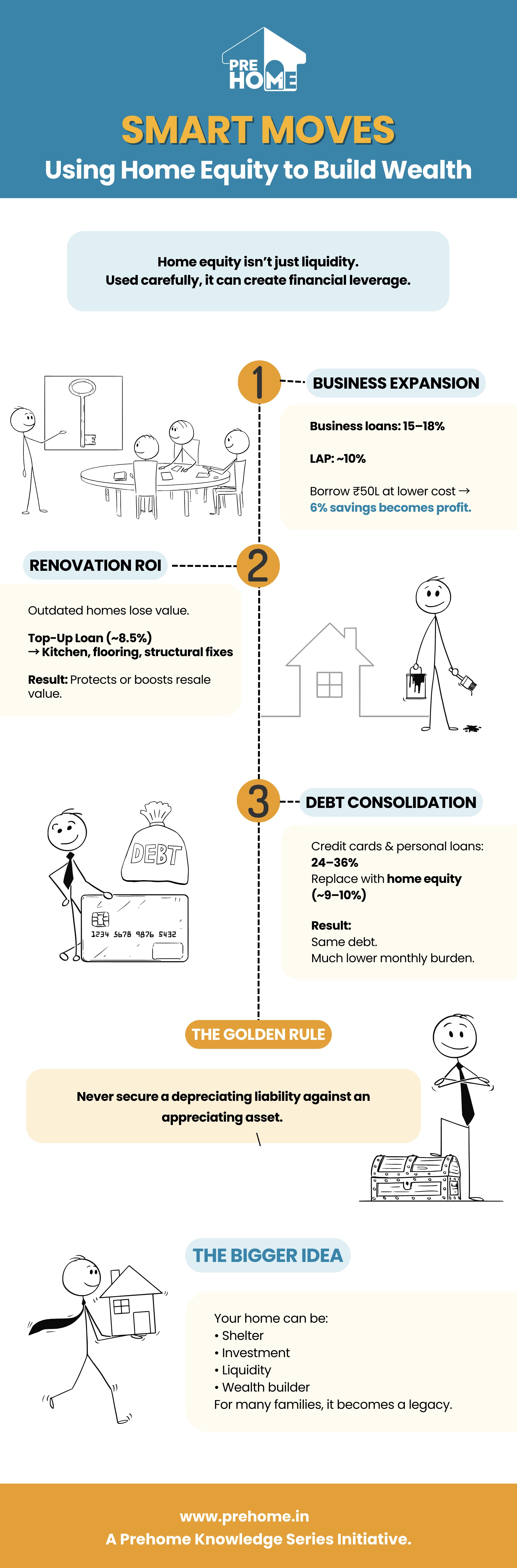

Getting working capital for a startup or growing business is challenging. Unsecured business loans often reach 15-18%.

Banks rarely grant LAP for early-stage startups. They prefer LAP when the borrower has a stable income or an established business.

In [Topic 12 - The Exit Strategy: Selling Your Home in India], we discussed how an outdated home loses value in the resale market.

High-interest debt is a serious financial issue.

There is one rule you must always follow when using home equity: Never secure a depreciating liability against an appreciating asset. Using a Top-Up loan to fund a luxury vacation or a lavish wedding puts your shelter at risk for a fleeting pleasure.

Your home can be a shelter, an investment, a source of cash, and even a way to build wealth. For many families in India, it eventually becomes something even more valuable - a legacy.

The real question isn't just about how you buy, live in, or leverage your home. It's about what will happen to it after you're gone.

Surprisingly, many homeowners make a significant mistake here. They think a nominee automatically gets ownership or that their children will "figure it out."

Sadly, property disputes in India don't usually start from bad intentions; they arise from unclear inheritance.

we will address the final phase of homeownership. Topic 14: Legacy & Succession — Passing It On. Why the difference between a Nominee and a Legal Heir can decide the future of your home.